{kind=link}

JAKARTA, Rafi Fadhilah — Indonesia is increasingly showing a market concentration pattern that gravitates toward two dominant players across multiple sectors. Some industries have already formed explicit duopolies, while others are heading toward “tight oligopolies” with similar competitive effects. This trend matters because it influences pricing, innovation, and the level of dependence MSMEs have on a small number of powerful platforms.

This article outlines the key sectors experiencing market consolidation, the underlying reasons Indonesia tends toward duopolistic structures, and the implications for the digital economy and initiatives such as the Indonesia Open Network (ION).

Sectors Showing Duopoly and Market Concentration in Indonesia

1. Ride-Hailing and Delivery

The market has effectively narrowed to two major platforms: Grab and Gojek/GoTo. Data from Euromonitor cited by Reuters suggests that a merger between them could create a combined market share of over 91% practically approaching monopoly territory, with the remainder taken by players such as Maxim.

With market power concentrated in only a few players, pricing and contractual terms may gradually reflect the strategic priorities of the leading platforms.

2. E-Commerce Marketplaces

A survey by the Indonesian Internet Service Providers Association (APJII) through the Indonesia Internet Profile 2025 report shows that Shopee is the most frequently accessed online shopping platform.

Shopee captured 53.22% of user access in 2025, rising sharply from 41.65% in 2024. TikTok Shop ranked second with 27.37%, also growing rapidly from 12.20% the previous year. Tokopedia followed with 9.57%, making Shopee the most preferred platform across demographic groups.

3. Telecommunications (Mobile)

Telkomsel and Indosat remain the two players most influential in shaping competition. According to the Oxford Business Group, Telkomsel holds around 63% market share, while Indosat accounts for 20%. Together, they control 83% of the market, giving them decisive influence over pricing, bundling strategies, and distribution. Other players such as, XL Axiata and Smartfren, trail behind with approximately 12% and 5% respectively.

4. Domestic Airlines

Data from the Indonesia National Air Carriers Association (INACA) shows that Lion Air Group dominates domestic aviation with around 62% market share through Lion Air, Batik Air, Wings Air, and Super Air Jet.

Garuda Indonesia and Citilink hold around 27% combined. Although this is not a pure duopoly, it resembles a “one dominant, one secondary” structure that still limits consumer choice.

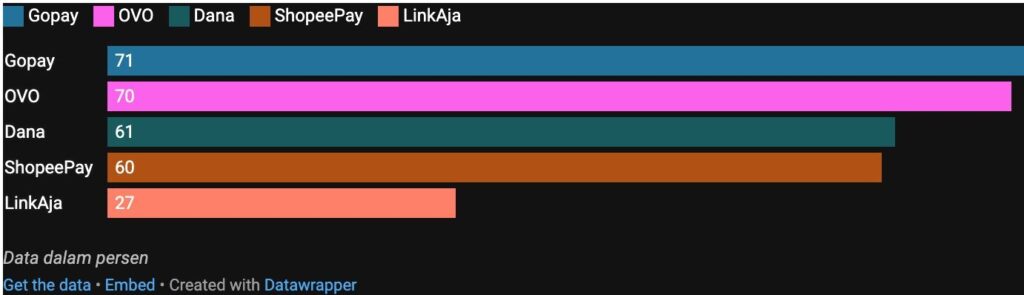

5. Digital Wallets and Payments

Digital wallets remain among the most popular fintech services in Indonesia, followed by digital banking and PayLater services. Their rapid growth is supported by rising online transactions, urban cashless habits, and encouragement from both government and private sector players.

Insight Asia’s E-Wallet Industry Outlook 2023 found that 74% of surveyed urban respondents had used a digital wallet. The platform percentages below reflect multi-usage, as most users have more than one e-wallet account, and the survey allowed multiple answers:

- GoPay: 71%

- OVO: 70%

- DANA: 61%

- ShopeePay: 60%

- LinkAja: 27%

However, Indonesia has a regulatory advantage. QRIS and BI-FAST create interoperability that reduces consumer lock-in and prevents dominant superapps from fully enclosing payment ecosystems.

6. Minimarkets / Offline Distribution

Among Indonesia’s many minimarket chains, Alfamart and Indomaret overwhelmingly dominate. Nielsen data shows the two control as much as 87% of the national minimarket market share.

This duopoly shapes access to shelf space, promotions, and FMCG supply chains, influencing both market pricing and manufacturer distribution strategies.

7. Instant Noodles / Fast-Moving Consumer Goods

MarketHac data shows that Indomie holds the largest share of the instant noodle category on e-commerce platforms with 59.29%, followed by Mie Sedaap at 18.97%.

This clearly reflects a duopoly in Indonesia’s staple instant noodle industry.

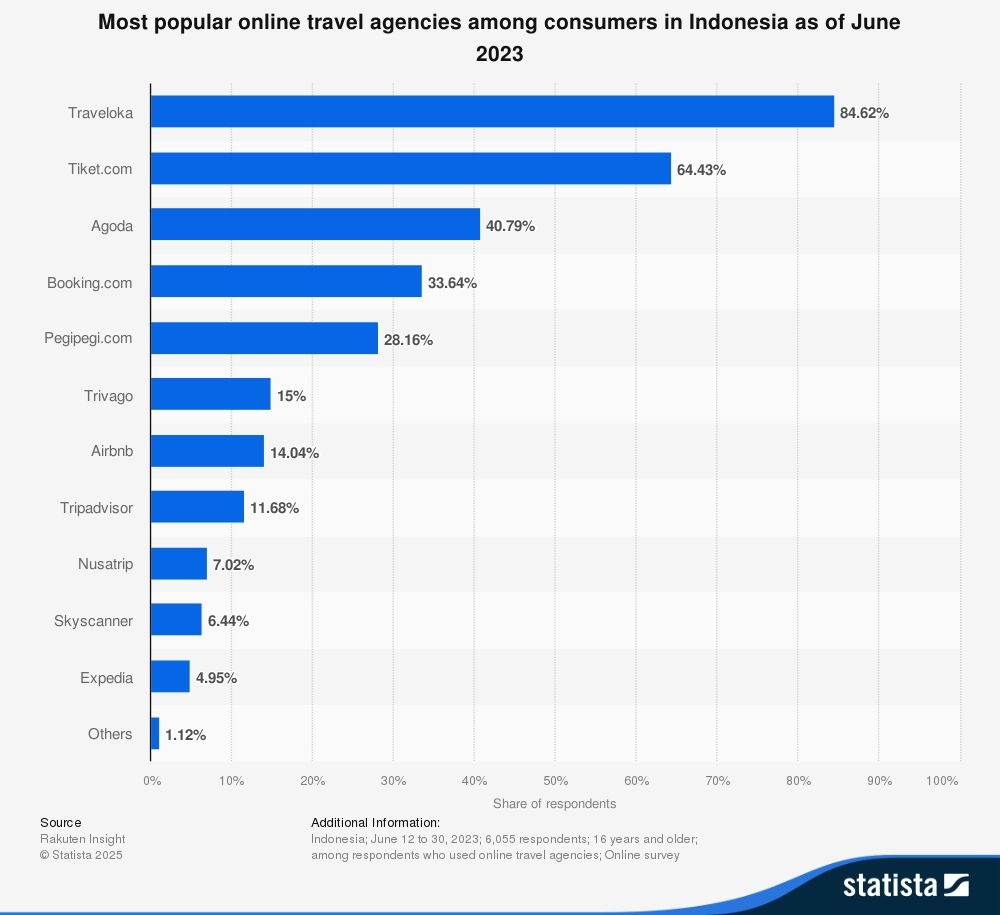

8. Online Travel and Ticketing

Indonesia’s OTA sector is widely recognized as being dominated by two major players: Traveloka and Tiket.com. Both offer comprehensive service ecosystems, strong brand recognition, and direct access to airline, hotel, and attraction inventories.

Statista data shows Traveloka leading the market, with Tiket.com forming a strong secondary player, creating a “soft duopoly” in the domestic OTA segment.

Why Indonesia Tends Toward Duopoly

- Archipelagic geography: High logistics and distribution costs allow large players to achieve scale advantages faster.

- Network effects: Superapps, digital wallets, marketplaces, and telcos all become more powerful as their user bases grow.

- Capital intensity & regulation: Sectors such as spectrum allocation, aviation, clearing/settlement systems, and major infrastructure favor a limited number of scaled operators.

Implications for Indonesia

As markets narrow to only two dominant players, competitive dynamics shift significantly. Pricing power generally moves in a direction unfavorable to consumers and businesses, with service fees, commissions, and take rates stabilizing at high levels or slowly increasing due to weak competitive pressure.

Innovation also changes course. Instead of focusing on user-choice-driven offerings, major platforms concentrate on strengthening internal efficiencies and unit economics. As a result, new features tend to reinforce monetization and retention, rather than expanding consumer or MSME alternatives.

For MSMEs, this creates deeper dependency. To gain traffic, process payments, or manage logistics, they must operate within the rules of one or two dominant platforms. Limited distribution options weaken their bargaining position and restrict their ability to negotiate better terms.

High market concentration also creates systemic risks. A disruption within one dominant player, whether from system outages, policy changes, or operational issues, can immediately affect commerce flows, mobility, or supply chains, as there are no sufficiently strong alternatives to absorb the impact.

In other words, duopoly is not merely about fewer choices for consumers; it represents a structural vulnerability across Indonesia’s digital economy.

What to Expect in 2026

The year 2026 will be pivotal for understanding the direction of digital competition and regulatory frameworks in Indonesia. One major issue is the potential alliance or partnership between Grab and GoTo. Should the initiative move forward, the government is expected to consider safeguards such as golden shares or special conditions to ensure that competition remains viable.

Meanwhile, KPPU continues monitoring the TikTok–Tokopedia merger through June 2027. This oversight is crucial for preventing anticompetitive behavior in logistics, supply chains, and merchant traffic allocation.

Another important development is the potential expansion of interoperability principles, proven successful through QRIS and BI-FAST, into other concentrated sectors such as logistics, e-commerce catalog systems, and data portability. Such policies could break existing bottlenecks, dilute gatekeeper power, and give new entrants more room to grow.

In short, 2026 will determine whether Indonesia continues down the path of consolidation or moves toward a more open and competitive digital ecosystem.

Conclusion

Indonesia’s market structure is increasingly concentrated, with many strategic sectors dominated by two or three major players. From telecommunications and e-commerce to ride-hailing, logistics, minimarkets, and online travel, the dominant pattern points to duopoly and tight oligopoly. This trend stems from structural factors such as geography, heavy investment requirements, strong network effects, and regulatory barriers.

The impacts are wide-ranging: pricing power shifts upward, innovation becomes inward-oriented, MSMEs rely more heavily on dominant platforms, and systemic risks escalate when one major player experiences disruptions.

Entering 2026, the trajectory of Indonesia’s digital competition landscape will hinge on three key developments: the potential Grab–GoTo partnership, KPPU’s ongoing oversight of TikTok–Tokopedia, and the possible expansion of interoperability regulations beyond payments. If policy decisions successfully open access and reduce reliance on digital gatekeepers, Indonesia could move toward a more inclusive and competitive ecosystem.

Ultimately, Indonesia’s challenge is not merely building large players but ensuring that their dominance does not hinder market dynamism. Maintaining fair competition, expanding interoperability, and lowering entry barriers will be essential to establishing a more balanced and sustainable digital economy.